Part 1 in our series of blogs on 'Cashless Khayelitsha' - our new pilot action-research project

Cashless Khayelitsha – Part 1: Driving adoption of digital payment solutions in township-based economies

03

May

2021

Posted by: Jessica Robey

Category:

Cashless Khayelitsha, Credit, Financial services, Social initiatives

No Comments

In South Africa, financial inclusion among individual consumers is high; according to Mastercard’s Impact of Innovation study, 77% of South African adults had a bank account in 2015 [1,2]. Despite this, cash remains king, particularly in lower income segments of the market. In the same study, Mastercard reports that cash transactions accounted for over 50% of the total value of consumer transactions in South Africa in 2015 and, in 2017, 90% of informal businesses were operating on a cash-only basis despite a high level of consumer interest in transacting digitally [1,2].

Why it matters

There is real benefit in digitising payments for economic development and growth. Not only are digital payments less costly than cash, they leave a visible footprint, enabling third parties (including lenders and taxation authorities) to track business activity accurately in close to real time. While some business owners might prefer their activities to remain below the radar, others see real benefit. Many township-based business owners we have interviewed are aware of the benefits digital payments offer their businesses. Reducing the risk of holding cash is top of mind for many. “I would feel much more safer having less cash or no cash at all in my store”, one business owner from Khayelitsha told us. Other business owners mentioned that providing their customers with the option to transact digitally would increase their daily sales. Some noted that customers were already asking to pay them digitally. Beyond this, these business owners would be able to share verified data with lenders, improving their chances of accessing business loans.

There is increasing interest in digitising small and micro-enterprises across the developing world. Nigeria, for instance, launched its Cash-less policy in 2012. As part of that, the Nigerian Inter Bank Settlement System (NIBBS), Nigeria’s central switch, launched an online, real time payment platform enabling financial institutions to offer low-cost instant transfers priced at between N10 (R0.37) and N50 (R1.87*) per transaction. Likewise, as part of the Cashless India initiative to drive adoption of digital payments in that country, the government subsidised merchant fees on small transactions.

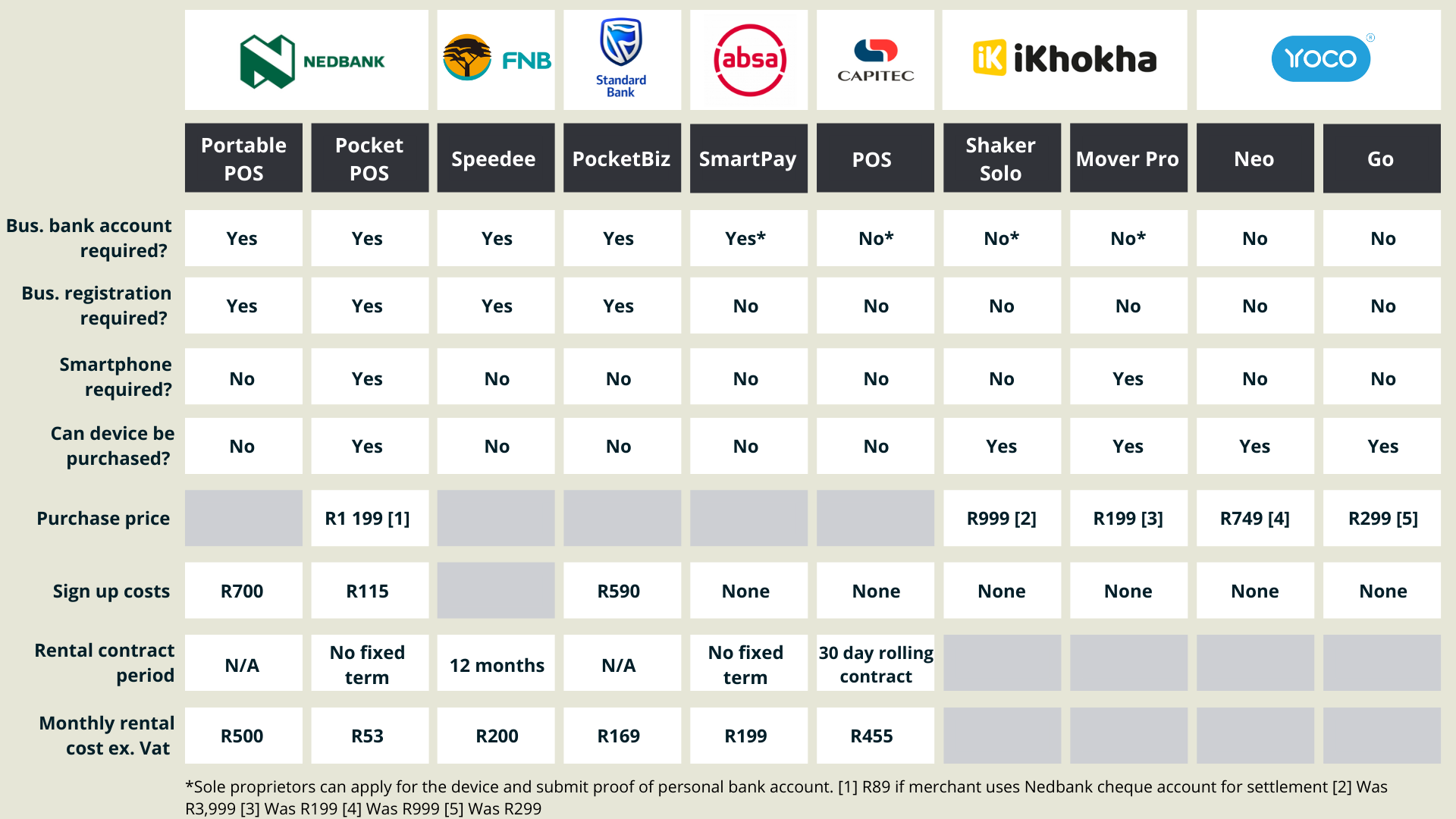

In South Africa, while the Reserve Bank’s vision 2025 identifies digital financial inclusion as a priority, progress on this is slow. It is also well-documented that mobile money has failed to take off in the country despite various solutions having been launched in the past by providers including Vodacom and MTN. In part this may be due to the card-based solutions which dominate the payment space in South Africa, despite their relatively high costs (see Table 1). However, the tides may be changing. A number of innovative mobile point of sale solutions have come to market recently, including Yoco and iKhoka which offer solutions tailored for small and micro enterprises. These providers offer a much simpler and streamlined sign up process and low upfront costs. However, their transaction fees can be higher than some of the traditional bank payment offerings. Yoco, in particular, has asserted dominance in the SME sector in South Africa, but there is opportunity to improve access and adoption of the solutions, and others, in township-based economies.

*Using the prevailing exchange rate of N26,75 to the Rand as reported by Morningstar on 21 April 2021

Table 1: Cost of selected digital payment devices in South Africa

Table 2: Transaction fees of selected digital payment devices

Finding opportunity in a crisis

The COVID-19 pandemic also provided an unexpected opportunity to accelerate progress towards cashless societies. In many countries, policymakers specifically promoted the adoption of digital payments solutions during the pandemic due to the risks associated with handling cash. According to the GSMA Covid-19 Mobile Money Response Tracker, 15 countries in Sub-Saharan Africa waived mobile money fees in order to encourage digital payments over cash transactions as a response to the pandemic [3]. Two of the countries include Rwanda and Kenya, which both saw significant increases in the number of mobile money transactions during this time [4]. Other popular policy responses included increasing transaction and balance limits and flexible KYC and onboarding. In contrast, South Africa’s COVID-19 response was to compel banks to enforce social distancing in queues and provide sanitiser at every ATM [5].

There is no doubt that policymakers and regulators in South Africa need to do more. But at the same time, there is scope for private sector providers to encourage adoption of available solutions in businesses that operate in cash.

Understanding the barriers to adoption and usage of digital payment solutions

In our recent engagements with business owners in Khayelitsha, most were generally unaware of the different digital payment solutions; some had never heard of providers like SnapScan, Yoco and iKhokha. This lack of awareness undoubtedly contributes to low levels of digital payment adoption by businesses.

There are quite possibly several other factors that limit the adoption of digital payment solutions, both on the merchant and customer side. It is critical that we identify these barriers and close the gap between the payment solutions businesses need to enable growth and the solutions that are available. This is what we aim to explore in our Cashless Khayelitsha pilot project.

As part of the pilot, we have started to work closely with five small businesses based in Khayelitsha, including food stands, a metal worker and an internet cafe, to assist them with the adoption of a digital payment solution. As part of the project we will apply for a card machine and a QR code-based solution such as SnapScan for each business owner. Over the course of the pilot, we will explore the experience from the application stage through to deployment of the device in the business, identify any challenges the business experiences in using the device and document the service and training offerings of the different providers. We will also work closely with business owners to monitor transactions and explore customer willingness to pay digitally. Over the longer term we would also like to establish whether adoption of digital payment solutions enables the businesses to access credit.

[1] 2019. The Future of Digital Payments in South Africa. https://www2.deloitte.com/content/dam/Deloitte/za/Documents/za-The-future-of-payments-in-South-Africa.pdf (Accessed 23/03/2021).

[2] Elliot, M. 2018. Driving Mobile and Card Acceptance Among Informal Retailers holds the Key to Scaling Cashless Payments in South Africa. https://newsroom.mastercard.com/mea/2018/11/27/driving-mobile-and-card-acceptance-among-informal-retailers-holds-the-key-to-scaling-cashless-payments-in-south-africa/ (Accessed 23/03/2021).

[3] https://www.gsma.com/mobilefordevelopment/programme/mobile-money/gsma-mobile-money-regulatory-response-to-covid-19-tracker-and-analysis/

[4] The Economist. 2020. The COVID-19 Crisis is Boosting Mobile Money. https://www.economist.com/middle-east-and-africa/2020/05/28/the-covid-19-crisis-is-boosting-mobile-money (Accessed 24/03/2021).

[5] Business Insider SA. 2021. Banks Respond to Government Demand for Sanitiser at Every ATM. https://www.businessinsider.co.za/banks-respond-to-government-demand-for-sanitiser-at-every-atm-2021-1 (Accessed 24/03/2021).

[6] 2017. Low Card Acceptance at Informal Enterprises Despite High Consumer Demand – Mastercard Research. https://newsroom.mastercard.com/mea/press-releases/low-card-acceptance-at-informal-enterprises-despite-high-consumer-demand-mastercard-research/ (Accessed 24/03/2021).

Authors: Illana Melzer, Jessica Robey, Frances Whitehead & Sarina Mpharalala

Like our blogs? Subscribe to receive email updates when new blogs are published.